Irv Blackman

Irv BlackmanThe R & D Tax Credit— How to Lower Your Income-Tax Bill

October 1, 2013Comments

Sometimes the Internal Revenue Code giveth more than it taketh. Section no. 41 of the code creates the Research and Development Tax Credit, designed to be your tax pal. But he’s a complicated fella.

Here’s why no. 41 is such a good tax friend: It allows you to gain two tax advantages—a deduction and a credit—for a single expenditure. For example, say you spend $1000 for wages on a qualified R & D project. First, you get a $1000 deduction; second, you use the same $1000 to make a calculation that gives you a credit, which can be deducted dollar-for-dollar to reduce your income-tax liability.

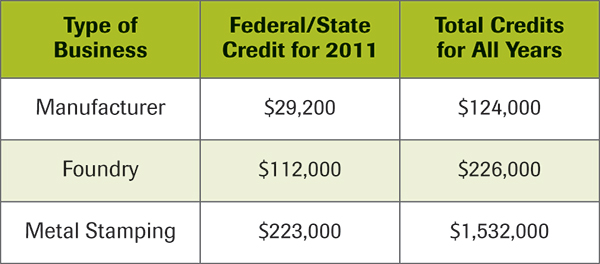

The R & D credit has been around since 1981. Many states have joined the tax-saving fun, awarding companies a credit on their state tax bill. The credit is available to every type of entity—S and C corporations, LLCs, partnerships, etc.

In a nutshell, the R & D tax credit applies to any company that makes, improves or develops products, software or processes—every-day stuff, not just scientists or engineers working in a laboratory.

When you consider getting into the R & D credit game, you must assess two factors:

• Do qualifying activities/projects take place, and

• What amount of qualifying expenses do you incur?

Your company is in if you perform any of the following activities:

• Develop/improve/test new concepts and/or technology

• Certification testing

• Manufacture products

• Create new, improved or more reliable products, formulas or processes

• Create prototypes or models, including computer-generated models

• Automate, streamline or improve internal processes

• Develop or improve production, manufacturing processes, software or hardware

• Add or improve equipment

• Try using new materials

• Design new or improved tools, dies, molds or other devices, or

• Hire outside consultants or contractors to do any of the above.

Podcast

Podcast